How Payment Gateways Work With Banks and Merchants

Online payments may look simple on the surface, but behind every successful transaction is a highly coordinated system involving multiple parties. When a customer enters their card details and clicks pay, a digital chain reaction begins that connects merchants, banks, and secure networks. This entire process is made possible through payment gateways, which serve as the bridge between businesses and financial institutions.

For merchants, accepting payments efficiently is critical to maintaining customer trust and ensuring smooth operations. For banks, validating and authorizing transactions is essential to prevent fraud and maintain financial security. Payment gateways sit in the middle, facilitating communication and ensuring that every transaction is processed accurately and securely.

Understanding how payment gateways work with banks and merchants is important for both business owners and everyday users. It helps businesses choose the right payment infrastructure and enables customers to better understand how their money moves digitally. From encryption to authorization and final settlement, every step plays a vital role in ensuring a seamless transaction experience.

This article explains the entire ecosystem in a clear and informative way. It breaks down the process step by step while also exploring key concepts, comparisons, and practical insights that define modern payment systems.

How Payment Gateways Work: Understanding the Core Concept

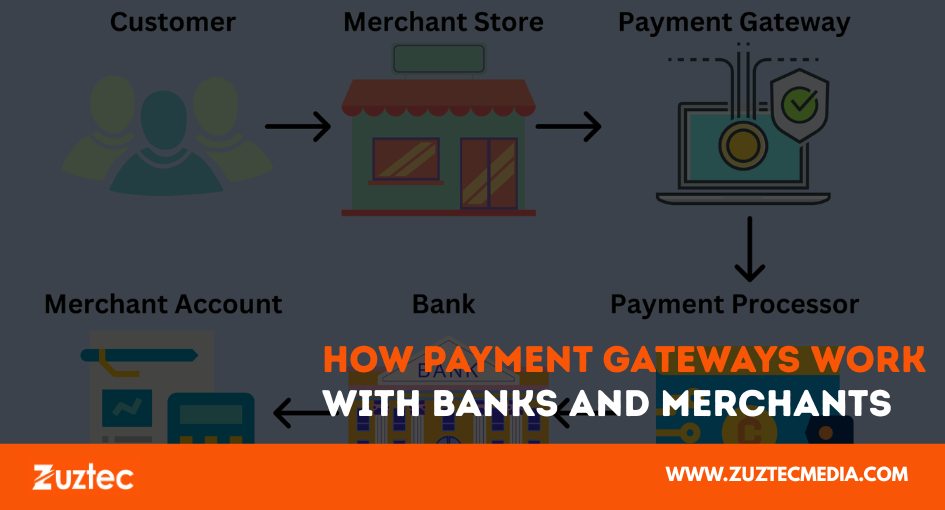

To begin with, it is important to understand what are payment gateway systems and why they are essential. A payment gateway is a secure technology that captures customer payment details and transmits them to the acquiring bank. It acts as a digital checkpoint that ensures all information is protected and properly routed.

Whenever a customer makes a purchase online, the gateway encrypts sensitive data such as card numbers. This ensures that the information cannot be intercepted by unauthorized parties. The gateway then forwards this data to the appropriate financial institutions for verification and approval.

The Connection Between Merchants and Banks

Payment gateways serve as a middleman between banks and retailers. Without them, businesses would need to connect directly with multiple financial systems, which would be complex and inefficient.

Merchants integrate payment gateways into their websites or apps to accept payments. Once a customer initiates a transaction, the gateway sends the request to the acquiring bank. This bank then communicates with the issuing bank, which verifies whether the customer has sufficient funds and whether the transaction is legitimate.

This seamless communication ensures that transactions are processed within seconds, even though multiple systems are involved.

Step-by-Step Transaction Journey

The process of how payment gateways work with banks and merchants can be broken down into clear steps:

First, the customer initiates a transaction by entering payment details.

Second, the gateway encrypts this data to ensure security.

Third, the information is sent to the acquiring bank.

Fourth, the acquiring bank forwards the request to the card network and issuing bank.

Fifth, the issuing bank verifies the transaction and either approves or declines it.

Finally, the response is sent back through the same chain to the merchant and customer.

After approval, the settlement process begins, where funds are transferred to the merchant account.

Different Structures in the Industry

There are several types of payment gateway solutions available, each designed for different business needs. Some gateways redirect customers to secure external pages, while others allow businesses to host payment forms directly on their websites.

Advanced systems use APIs to provide full customization, allowing businesses to create seamless checkout experiences. The choice depends on factors like business size, technical capability, and customer expectations.

Key Roles in the Ecosystem

Banks play a crucial role in ensuring transaction security. The issuing bank verifies the customer’s account, while the acquiring bank processes the payment on behalf of the merchant.

Merchants are responsible for integrating secure payment systems and ensuring compliance with industry standards. Payment gateways simplify this responsibility by handling encryption and communication.

Together, these entities create a reliable system that supports digital commerce.

Comparing Related Systems

Many people confuse gateways with processors, but there is a clear distinction in the payment gateway vs payment processor comparison.

A payment gateway focuses on securely transmitting data from the customer to the bank. A payment processor, on the other hand, handles the actual movement of funds between banks.

Both systems are essential and work together to complete a transaction successfully.

FAQs

What is the best payment method to not get scammed?

Credit cards and trusted digital wallets are generally the safest options because they offer strong fraud protection and dispute resolution features. These methods allow users to reverse unauthorized transactions more easily. Avoid sending money directly through bank transfers to unknown individuals, as these are harder to recover.

How does a payment gateway make money?

Payment gateways generate revenue by charging transaction fees, setup fees, or monthly subscription costs. They may also take a small percentage of each processed payment. Additional services like fraud detection and reporting tools can also contribute to their earnings.

Is Zelle a payment gateway?

Zelle is not a payment gateway. It is a peer-to-peer payment service that allows users to transfer money directly between bank accounts. Payment gateways are designed for businesses to securely accept payments from customers.

What are the risks of using a payment gateway?

Risks include potential data breaches, fraud attempts, and system downtime. Although gateways use strong security measures, no system is completely risk-free. Choosing a reliable provider and following security best practices can significantly reduce these risks.

Can someone steal my money if they have my routing number and account number?

It is possible in some cases, but banks have strong monitoring systems to detect suspicious activity. Unauthorized transactions can often be reported and reversed. Regularly checking account activity and using secure payment methods helps minimize the risk.

Regional Perspective

When looking at how payment gateways work in USA, the system operates within a strict regulatory framework. Payment providers must comply with financial laws and security standards that protect consumers and businesses.

The US market is highly advanced, with gateways supporting multiple payment methods and currencies. Fraud prevention technologies are also widely used, ensuring secure transactions across different platforms.

Common Providers in the Market

There is a long list of payment gateway providers available globally. Some are designed for small businesses, while others cater to large enterprises handling high transaction volumes.

Businesses choose providers based on factors like fees, ease of integration, security features, and customer support. Selecting the right provider can significantly impact payment success rates and customer satisfaction.

Security and Trust Factors

The foundation of any payment system is security. Gateways use advanced encryption methods to protect sensitive data during transmission. They also implement tokenization, which replaces actual card details with secure tokens.

Fraud detection systems monitor transactions in real time, identifying unusual patterns and preventing unauthorized activities.

As cybersecurity expert Bruce Schneier said

“Security is not a product but a process.”

This reflects the continuous effort required to maintain safe and reliable payment systems.

Benefits for Modern Businesses

Payment gateways offer several advantages for merchants. They enable businesses to accept payments globally, improve checkout experiences, and reduce manual processing.

Customers benefit from fast and secure transactions, which increases trust and encourages repeat purchases. These advantages make payment gateways a critical component of modern commerce.

Challenges to Consider

Despite their benefits, payment gateways also present a number of practical challenges that businesses should not overlook. One of the most common concerns is transaction fees, which can gradually reduce profit margins, especially for small- and medium-sized businesses that operate on tight budgets. These fees may include setup costs, monthly charges, and a percentage of each transaction, making it important to fully understand the pricing structure before choosing a provider.

Another challenge is technical integration. While many gateways offer user-friendly solutions, more advanced or customized systems often require developer support. This can increase initial setup time and cost, particularly for businesses that want a seamless checkout experience or need to integrate with existing platforms.

Security risks also remain a concern. Although payment gateways use strong encryption and fraud detection tools, cyber threats continue to evolve. Businesses must ensure they follow best practices such as maintaining secure websites, updating systems regularly, and complying with industry standards to protect customer data.

In addition, occasional system downtime or payment failures can impact customer experience and lead to lost sales. Even short disruptions during peak times can affect trust and revenue. Businesses should look for providers with high reliability, strong support, and backup systems to minimize such risks.

To overcome these challenges, businesses need to carefully evaluate payment gateway providers, compare features and costs, and invest in secure and scalable solutions that support long-term growth.

In the end, learn how payment gateways work: payment gateways play a vital role in connecting merchants and banks, ensuring that every online transaction is processed securely and efficiently. From encrypting customer data to enabling communication between financial institutions, they make digital payments fast and reliable. By understanding how these systems work, businesses can choose better solutions, and customers can feel more confident when making online purchases.